Justice is Not an Asset Class

Note: I published this originally way back in November 2014, so all the references are a bit dated. But I think the basic message is still relevant, especially to legal startups.

Yesterday witnessed the bold, bright launch of a startup named LexShares, an online marketplace for investing in commercial litigation. Its well-executed media assault included a bunch of synchronous stories in TechCrunch, The Next Web, Forbes, Wall Street Journal, Boston Globe and elsewhere.

LexShares is led by a former investment banker and an attorney/entrepreneur/litigation finance expert. It’s backed by prominent Boston VC firm Atlas Venture, which invests in a lot of great companies.

I’m generally supportive of new experiments in the legal field. I’m an avid student of different forms of crowdsourcing. I’ve got nothing against third-party litigation funding in principle. And I’m no pacifist when it comes to legal brawls.

But this launch gave me pause.

Long on Investment, Short on Justice

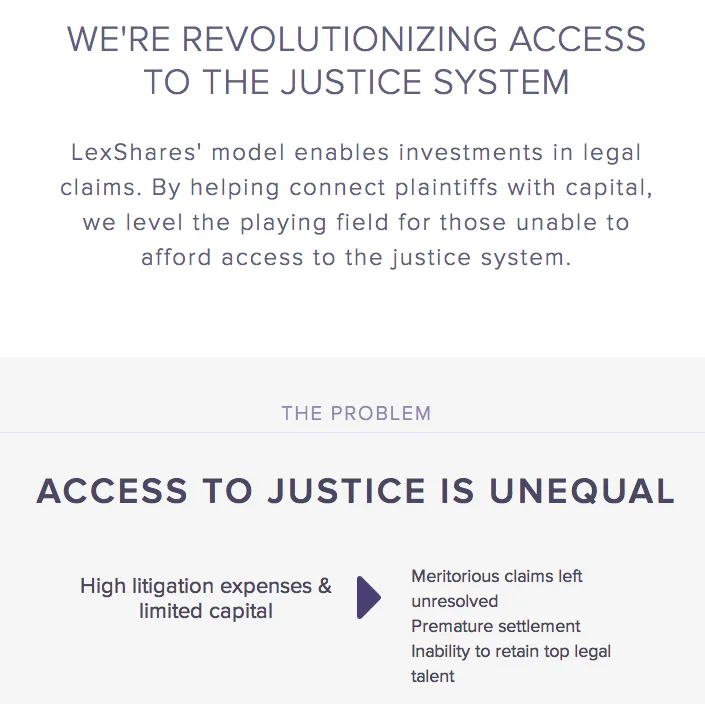

To hear the media and marketing pros behind LexShares tell it, what we have here is a justice savior. Now we shall have order, fairness, equality, transparency and democracy in our civil justice system. No longer shall the poor and vulnerable go unrepresented, their rights unprotected. No more shall equal justice be beyond our reach.

From LexShares’ How It Works page:

So noble. So generous. So brave. #InvestInJustice.

Yet I do not think “access to justice” means what LexShares thinks it means. In reality, access to justice is a huge, crushing crisis that afflicts millions of people and has nothing to do with lucrative suits for damages, alternative investment engineering or third-party litigation financing. To the contrary, the access to justice crisis exists because there is no financial incentive for anyone to help those in need.

In other words, if you happen to be running around with a damages claim in your pocket that is “meritorious” enough to attract investment from rational economic actors, access to justice is not one of your problems.

By the same token, LexShares has nothing to do with access to justice. It’s not a legal aid organization. It doesn’t do pro bono. It’s an investing marketplace that exists to make money for itself, its shareholders and presumably the investors whose money it hopes to attract.

Which is fine. LexShares doesn’t have to save the world or lift up the downtrodden. Accredited investors who want to give their money to plaintiff’s lawyers rather than startups, creators or charities are not at the top of my pity list. And there’s nothing wrong with making a buck off litigation. Lawyers do it all the time.

Just spare us the self-righteous marketing bunk.

Litigation Is For Losers

I’ve been fortunate to work with some devastatingly effective commercial litigators. These were skilled, seasoned artisans and operators who delivered exceptional outcomes.

One thing they all had in common is they went out of their way to explain to clients that litigation is usually a bad idea, that unexpected things happen routinely, and that even the most successful lawsuits are a massive distraction.

The truth is that lawsuits are miserable affairs. The “just” ones start, by definition, with unwanted injury. In the vast majority of cases, the best a plaintiff can hope for is a shot at being made whole, after being thoroughly deposed, cross-examined, threatened and discovered. All too often, plaintiffs regret the decision to sue, and not just because of costs.

For small companies and entrepreneurs, in particular, I can imagine very few circumstances that would make initiating a lawsuit a good business decision. Yet LexShares and its backers seem to relish the prospect of adding lawsuits to the founder’s toolkit:

Atlas Ventures partner Chris] Lynch sums it up with a line from Born in East L.A.: “F — me? No, f — you!”

“It’s the ultimate tool for the underdog,” he said. “Right now the big guys use the legal system to take advantage of entrepreneurs.”

I’m all for underdogs and toughness, but in what universe does an early stage investor want its small portfolio companies to be suing big corporations? And what kind of entrepreneur wants to be embroiled in a lawsuit — even a cost-free one — except as a last resort?

One thing all this bravado misses is that it’s often the little guy who gets sued. It’s Goliath v. David, not the reverse. Even when David strikes first and true, Goliath will counterclaim to put David at risk. It’s the first play in the playbook, believe me. And what ensues is a long, bloody, distracting battle that our hypothetical David opted into.

LexShares funds plaintiffs, not defendants, so it isn’t going to help David much in the Goliath v. David situation. Come to think of it, why would LexShares limit itself to funding only underdogs? If Goliath’s claim offered an attractive risk/reward profile, wouldn’t LexShares want to fund Goliath against David? And maybe Goliath isn’t a big corporation, but a patent troll stalking startups flush with VC cash. In the past, that has been quite a lucrative way to invest in justice, though it could be losing its appeal.

My point is that commercial litigation is always hard and ugly and mostly yields losers all around. At best, it’s agnostic about whether the winners are good guys or bad guys. I’ll be surprised if litigation investment proves to be any different.

The End of Lawsuits?

Some have hypothesized that LexShares “probably eliminates frivolous lawsuits.” That would be good of course.

Except that LexShares wants to increase “access to justice,” by which it means it wants to give plaintiffs more reasons to file lawsuits. That’s more lawsuits, not less. Even if LexShares funded only virtuous claims, how does that reduce frivolous claims? Now if LexShares were paying plaintiffs not to file their suits, we might be onto something.

I suppose the hypothesis might be that, at scale, the inability to raise money through LexShares could be a strong enough signal to potential plaintiffs that they’ll think twice about filing a lawsuit that can’t attract funding. I’m a skeptic for lots of reasons, but if it plays out that way, great. One thing I’ve noticed in my own litigation career is that frivolous claims and lucrative claims are not mutually exclusive.

The Ignorance of the Crowd

One other concern I have about crowdfunding litigation is the unavoidable lack of disclosure to, and thus ignorance of, the investing crowd.

I’m mostly in the camp of those who believe that accredited investors should be free to invest or spend their money however they like. If backing lawsuits is their thing, and there’s no outright fraud, then I’m not too worried.

But I do see a problem in that an investor’s interest in disclosure of material information about weaknesses in a claim is at odds with a plaintiff’s interest in concealing material information about weaknesses in a claim. Concerns about privilege waiver, legal ethics, confidentiality and discoverability heighten this conflict, although LexShares has taken care in trying to address these concerns.

Equally worrisome is the fact that the investor will have no access to the other party in the dispute. Or will LexShares’ due diligence include reaching out to the defendant for its side of the story?

All of which is to say that valuing legal claims is a very tricky, very uncertain business, especially when you have such limited access to the material facts.

A Thin Silver Lining

All that said, while this strikes me as a bad idea, that’s just my opinion, informed by a fair amount of experience deep in the trenches of the kind of litigation LexShares aims to fund.

I don’t presume to know how it will play out. I can imagine both spectacular failure and astounding success. I even can imagine this leading to interesting new roles for lawyers as investment advisers. It might also have a positive effect on the adoption of litigation analytics and other emerging disciplines that aim to systematize litigation. I’d welcome that.

At bottom, my strong negative reaction is mostly to the phony marketing of this as something more than a bold, cold, calculated play by sophisticated investment professionals who see an opportunity to take advantage of a new kind of market. As nothing more noble or righteous than that, I will be curious to see how it fares.